PERMANENT INSURANCE

Life Insurance is a core component of proper financial and wealth management planning.

Our team will assess your life insurance needs now and for the future. We will provide recommendations about the best choices and options available in the market today.

Life Insurance provides:

- Estate tax needs

- Tax deferral opportunities

- Wealth transfer

- Buy/Sell shareholder and partnership agreement funding

- Key person insurance

- Income replacement for family needs

CORPORATE OWNED LIFE INSURANCE

Life Insurance: Why would a business owner want it?

The traditional perception of life insurance is that it is a financial product providing income replacement at death, funding tax liabilities, partnership buyout agreements, covers key people in an organization or is used to equalize an estate.

Most ultra-high net worth Canadians are sufficiently self-insured by virtue of their assets. They feel, and rightly so, that they don’t need insurance for traditional risk mitigation purposes.

That said, corporate-owned life insurance could be used by wealthy individuals as a tax effective way to accumulate passive wealth inside a company, to access that wealth tax-free and to transfer it tax-free to surviving beneficiaries.

The Problem

In many businesses, the retained profits or surplus cash are invested in taxable investments. This is often the case when the business owner doesn’t need the extra income and has a higher marginal tax rate than their business. Consequently, they take advantage of the low corporate tax rates on active business income by saving money in their corporations, if they don’t require it for personal purposes. This accomplishes a tax deferral, but eventually these assets will come out of the corporation and be taxed at high dividend tax rates, depending on the taxpayer’s post mortem planning

The Solution

A solution to this problem is to invest some of the retained profits in tax-exempt permanent life insurance. There are two main benefits to making such an investment, namely:

- The savings component of the life insurance policy can grow on a tax-free basis; and

- A significant portion, if not all, of the policy proceeds payable at death can be paid to the shareholder’s estate as a tax-free capital dividend.

Other Income Tax Advantages of Corporate-Owned Life Insurance

One advantage of corporate-owned life insurance is that the premiums are paid with corporate after-tax dollars, which are taxed at a much lower tax rate than the individual shareholder’s personal tax rate. The corporate tax rate applicable to active business income in Ontario is approximately 15% and to investment income is 50%. The top individual marginal tax rate in Ontario is approximately 53.5%.

In addition to the foregoing, another advantage is that upon death, an individual is deemed to dispose of his/her property at its fair market value. As it pertains to shares of a corporation, which owns a life insurance policy, the Income Tax Act dictates to value the life insurance policy at its cash surrender value immediately before death. Typically, this value will be significantly less than the policy’s payout following death, as well as being significantly less than the value of the property that would have otherwise been accumulated by the corporation had it not purchased the life insurance policy. Consequently, purchasing life insurance can also assist to lessen the tax payable at death in respect of shares of a private corporation, since it will usually lead to a lower valuation for the corporate shares than had no life insurance been purchased.

LIVING BENEFITS

People are living longer and governments can no longer afford to take care of us, so we need to take more responsibility for our healthcare.

Our customized healthcare solutions include Critical Illness Insurance, Long Term Disability Insurance with High Limits and Long Term Care Insurance,

Living Benefits describes a group of insurance products that pay a benefit to the insured while alive:

- Long Term Disability Insurance with High Limits: protects you from the possible loss or reduction of income as a result of not being able to work due to a sickness, injury or disability. High-income earners can now get coverage of up to $75,000 per month, and sometimes more, in disability benefits.

- Critical Illness Insurance: provides up to $2 million of tax-free funds in the event of a critical illness such as cancer, stroke or heart attack. More than 2 dozen conditions can be covered.

- Long Term Care Insurance: provides tax-free funds of up to $10,000 per month for long-term care services in your home or in a long-term care facility.

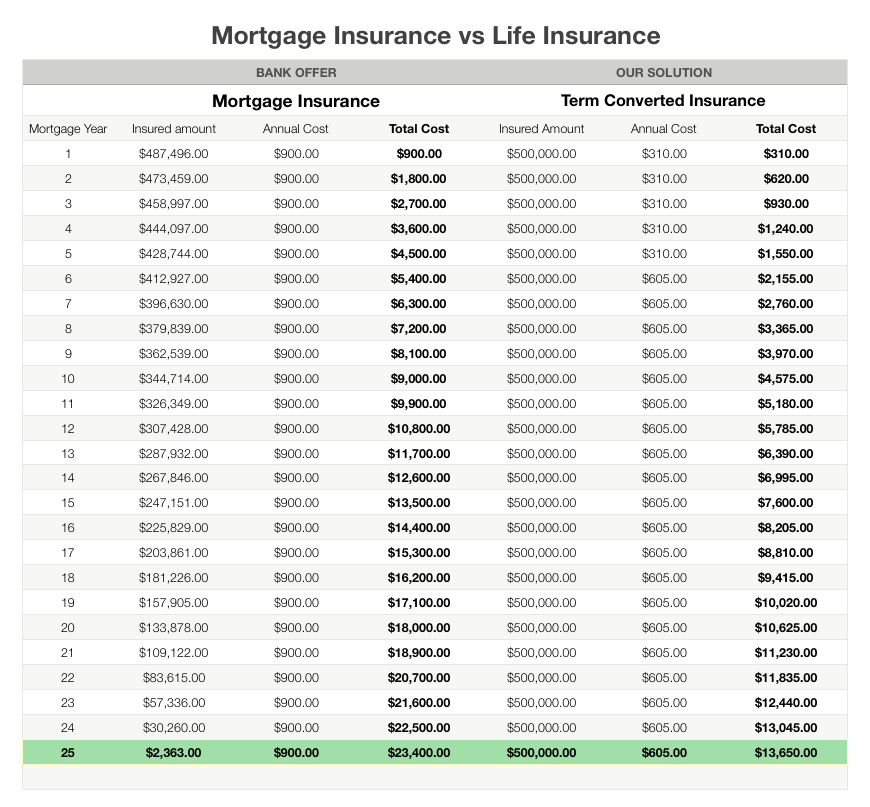

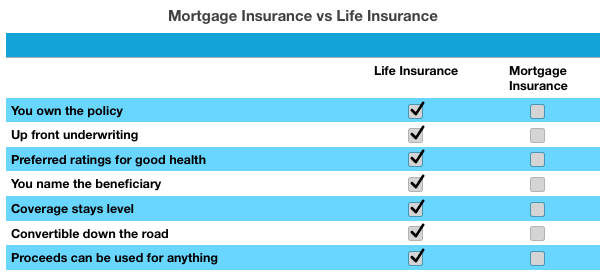

MORTGAGE INSURANCE VS LIFE INSURANCE

There are significant differences between mortgage insurance provided and owned by the bank, and life insurance owned by the lives insured. Below you will find a list of those differences and case example detailing the financials of a 35 year male purchasing a new home seeking a mortgage and coverage for $500,000.